All Categories

Featured

Table of Contents

The disadvantages of infinite financial are typically overlooked or otherwise stated at all (much of the information readily available regarding this principle is from insurance policy representatives, which may be a little prejudiced). Only the cash money worth is expanding at the reward rate. You additionally have to spend for the cost of insurance coverage, charges, and costs.

Business that supply non-direct recognition finances might have a lower reward price. Your money is secured into a complicated insurance policy item, and abandonment costs generally don't vanish till you have actually had the plan for 10 to 15 years. Every permanent life insurance policy is different, but it's clear somebody's total return on every buck invested in an insurance coverage item might not be anywhere near the returns price for the policy.

Infinite Banking Concept Reviews

To provide a really basic and theoretical example, let's think somebody is able to make 3%, on average, for every dollar they spend on an "unlimited banking" insurance coverage item (after all expenditures and charges). If we assume those dollars would certainly be subject to 50% in taxes complete if not in the insurance policy product, the tax-adjusted price of return could be 4.5%.

We presume higher than ordinary returns overall life product and an extremely high tax rate on bucks not take into the policy (which makes the insurance coverage item look far better). The fact for numerous individuals may be even worse. This pales in comparison to the lasting return of the S&P 500 of over 10%.

Unlimited banking is a great product for representatives that offer insurance coverage, yet may not be ideal when compared to the less costly alternatives (without any sales people making fat payments). Below's a break down of some of the other supposed benefits of limitless banking and why they may not be all they're split up to be.

How To Set Up Infinite Banking

At the end of the day you are buying an insurance coverage item. We enjoy the protection that insurance policy offers, which can be obtained much less expensively from a low-priced term life insurance coverage policy. Unpaid car loans from the policy might also minimize your survivor benefit, diminishing another level of security in the plan.

The principle only works when you not only pay the considerable premiums, but use added cash to purchase paid-up enhancements. The opportunity cost of every one of those dollars is significant exceptionally so when you can rather be spending in a Roth IRA, HSA, or 401(k). Even when compared to a taxable financial investment account and even a savings account, infinite financial may not offer similar returns (compared to spending) and similar liquidity, accessibility, and low/no fee structure (compared to a high-yield cost savings account).

With the increase of TikTok as an information-sharing platform, economic advice and methods have actually discovered a novel means of dispersing. One such technique that has actually been making the rounds is the unlimited financial concept, or IBC for short, garnering recommendations from celebrities like rap artist Waka Flocka Flame. Nonetheless, while the approach is presently preferred, its origins trace back to the 1980s when financial expert Nelson Nash presented it to the world.

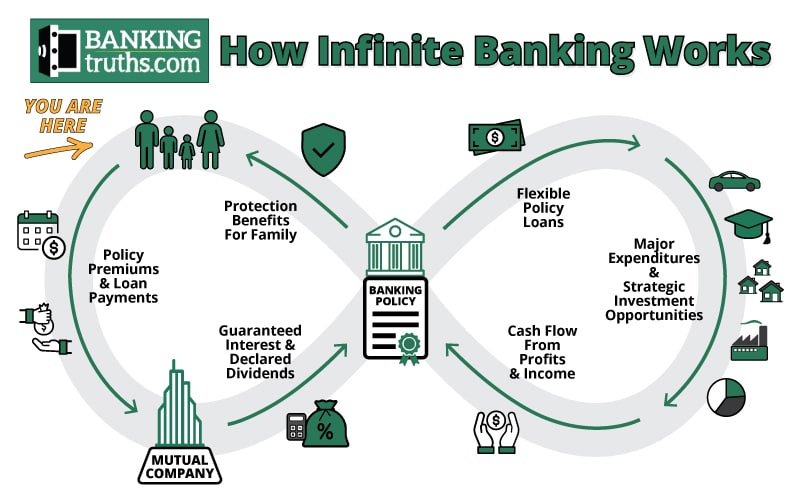

Within these plans, the cash money worth grows based upon a rate established by the insurance firm. As soon as a significant money worth gathers, policyholders can acquire a cash money value lending. These car loans vary from traditional ones, with life insurance working as collateral, meaning one could shed their insurance coverage if borrowing exceedingly without sufficient money worth to support the insurance policy costs.

Infinite Banking System Review

And while the attraction of these plans appears, there are natural limitations and threats, necessitating thorough money worth monitoring. The strategy's authenticity isn't black and white. For high-net-worth people or company proprietors, particularly those utilizing methods like company-owned life insurance policy (COLI), the advantages of tax obligation breaks and substance development can be appealing.

The attraction of boundless banking doesn't negate its obstacles: Cost: The fundamental demand, a permanent life insurance coverage plan, is costlier than its term equivalents. Qualification: Not everybody qualifies for whole life insurance due to rigorous underwriting procedures that can leave out those with certain health and wellness or way of living problems. Intricacy and risk: The detailed nature of IBC, combined with its threats, might hinder lots of, specifically when less complex and less dangerous choices are offered.

Allocating around 10% of your regular monthly income to the policy is just not viable for a lot of individuals. Component of what you check out below is just a reiteration of what has actually currently been stated above.

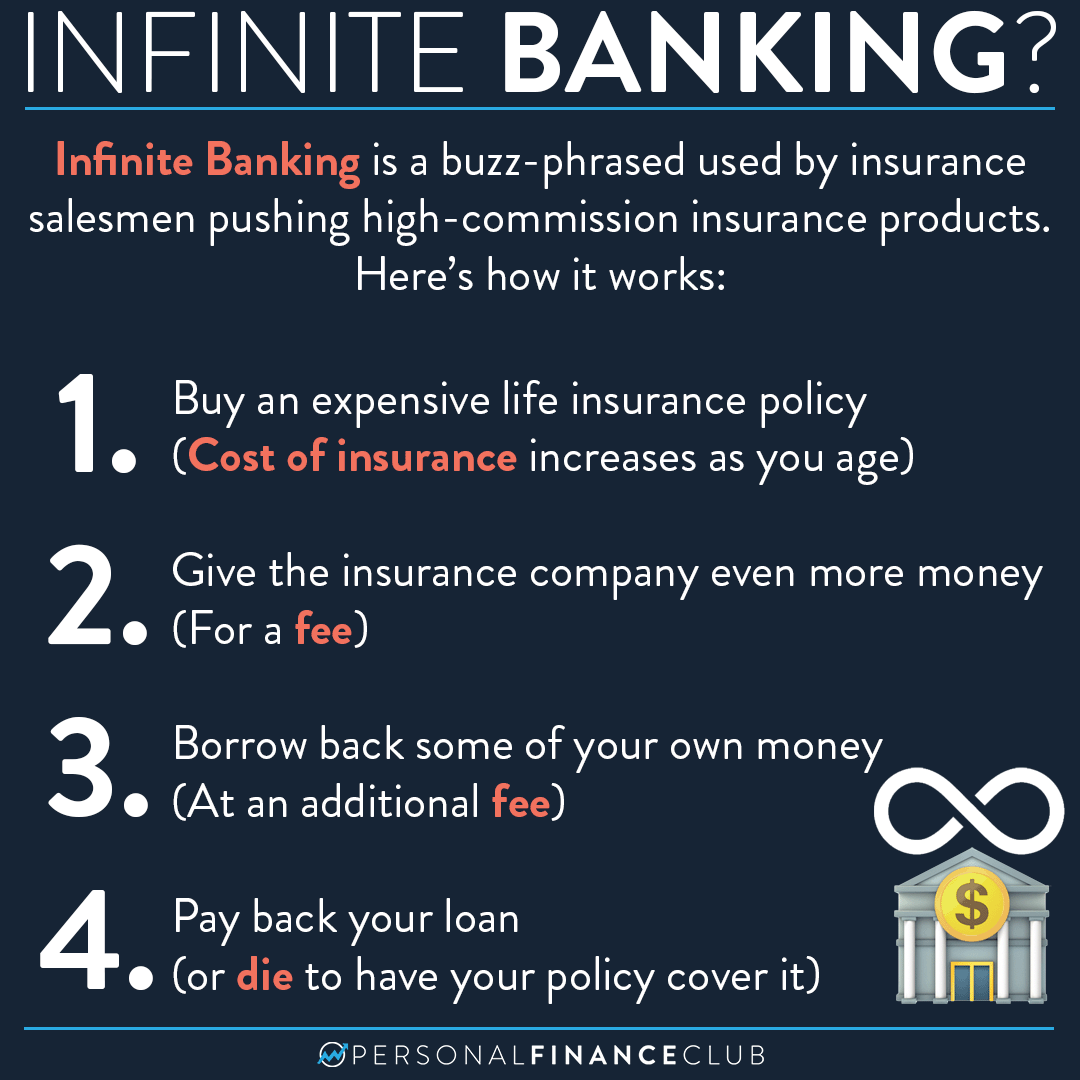

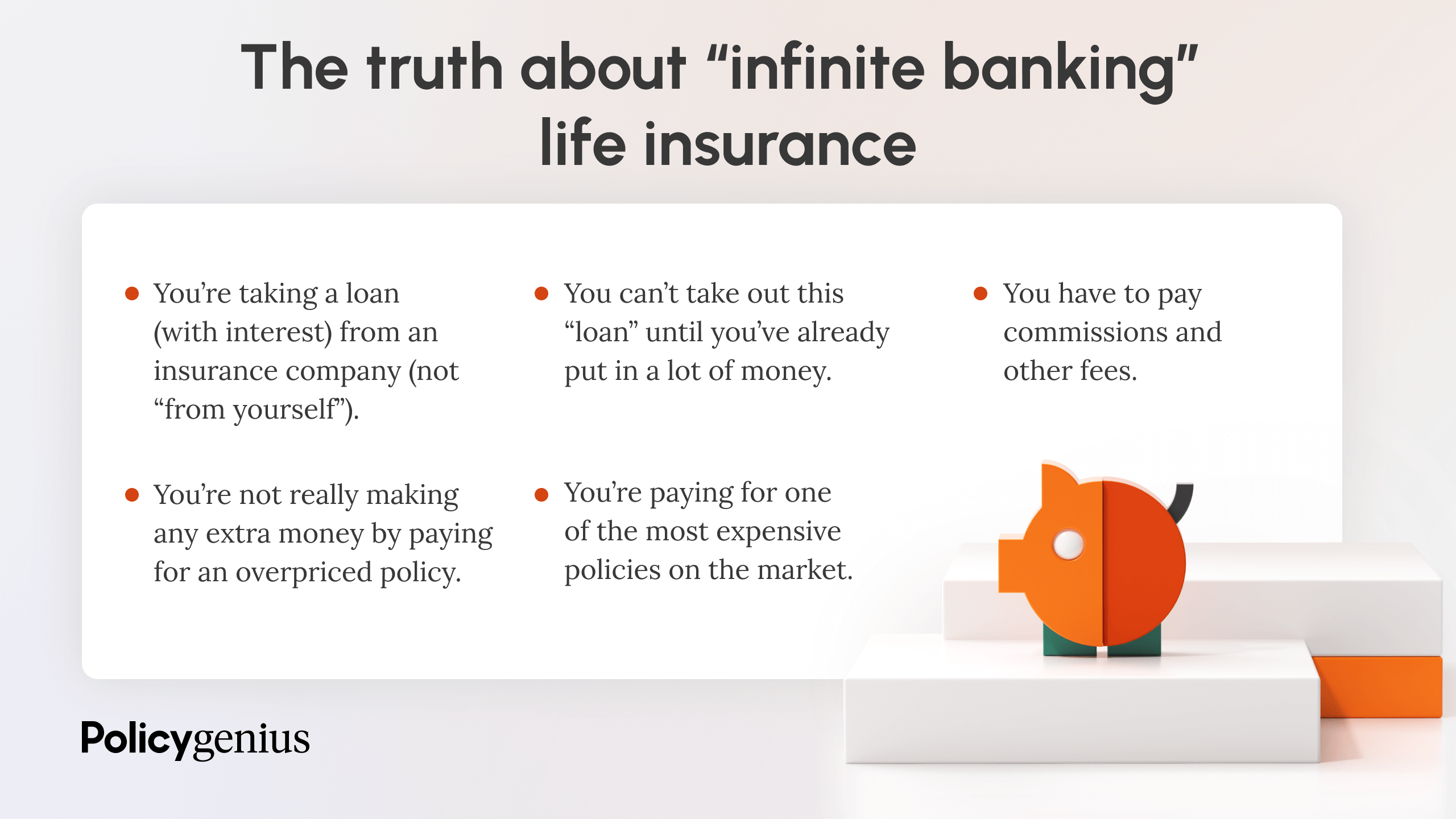

So prior to you obtain into a circumstance you're not prepared for, understand the complying with first: Although the concept is frequently offered thus, you're not really taking a funding from on your own - infinite banking wiki. If that held true, you wouldn't have to settle it. Rather, you're obtaining from the insurer and need to repay it with passion

Infinite Banking System Review

Some social media articles suggest using money value from entire life insurance to pay down credit score card debt. When you pay back the lending, a section of that rate of interest goes to the insurance firm.

For the first several years, you'll be paying off the payment. This makes it exceptionally challenging for your plan to build up worth during this time. Unless you can afford to pay a few to several hundred dollars for the following decade or more, IBC will not function for you.

If you require life insurance coverage, right here are some important pointers to think about: Think about term life insurance. Make sure to shop around for the ideal rate.

Unlimited financial is not a product and services supplied by a certain establishment. Limitless financial is an approach in which you buy a life insurance coverage plan that builds up interest-earning money value and secure fundings versus it, "borrowing from yourself" as a source of funding. Then eventually pay back the loan and begin the cycle around once more.

Pay policy costs, a part of which constructs cash worth. Take a loan out versus the policy's money worth, tax-free. If you use this principle as intended, you're taking money out of your life insurance coverage policy to buy everything you 'd need for the rest of your life.

{kind=link}

Latest Posts

Become Your Own Bank, Hampton Author Advises In 'The ...

Nelson Nash Life Insurance

Become Your Own Bank. Infinite Banking